Authored by Gail Tverberg via Our Finite World blog,

Most of us are familiar with the Politically Correct (PC) World View. William Deresiewicz describes the view, which he calls the “religion of success,” as follows:

There is a right way to think and a right way to talk, and also a right set of things to think and talk about. Secularism is taken for granted. Environmentalism is a sacred cause. Issues of identity - principally the holy trinity of race, gender, and sexuality - occupy the center of concern.

There are other beliefs that go with this religion of success:

- Wind and solar will save us.

- Electric cars will make transportation possible indefinitely.

- Our world leaders are all powerful.

- Science has all of the answers.

To me, this story is pretty much equivalent to the article, “Earth Is Flat and Infinite, According to Paid Experts,” by Chris Hume in Funny Times. While the story is popular, it is just plain silly.

In this post, I explain why many popular understandings are just plain wrong. I cover many controversial topics, including environmentalism, peer-reviewed literature, climate change models, and religion. I expect that the analysis will surprise almost everyone.

Myth 1: If there is a problem with the lack of any resource, including oil, it will manifest itself with high prices.

As we reach limits of oil or any finite resource, the problem we encounter is an allocation problem.

Figure 1. Two views of future economic growth. Created by author.

As long as the quantity of resources we can extract from the ground keeps rising faster than population, there is no problem with limits. The tiny wedge that each person might get from these growing resources represents more of that resource, on average. Citizens can reasonably expect that future pension promises will be paid from the growing resources. They can also expect that, in the future, the shares of stock and the bonds that they own can be redeemed for actual goods and services.

If the quantity of resources starts to shrink, the problem we have is almost a “musical chairs” type of problem.

Figure 2. Circle of chairs arranged for game of musical chairs. Source

In each round of a musical chairs game, one chair is removed from the circle. The players in the game must walk around the outside of the circle. When the music stops, all of the players scramble for the remaining chairs. Someone gets left out.

The players in today’s economic system include

- High paid (or elite) workers

- Low paid (or non-elite) workers

- Businesses

- Governments

- Owners of assets (such as stocks, bonds, land, buildings) who want to sell them and exchange them for today’s goods and services

If there is a shortage of a resource, the standard belief is that prices will rise and either more of the resource will be found, or substitution will take place. Substitution only works in some cases: it is hard to think of a substitute for fresh water. It is often possible to substitute one energy product for another. Overall, however, there is no substitute for energy. If we want to heat a substance to produce a chemical reaction, we need energy. If we want to move an object from place to place, we need energy. If we want to desalinate water to produce more fresh water, this also takes energy.

The world economy is a self-organized networked system. The networked system includes businesses, governments, and workers, plus many types of energy, including human energy. Workers play a double role because they are also consumers. The way goods and services are allocated is determined by “market forces.” In fact, the way these market forces act is determined by the laws of physics. These market forces determine which of the players will get squeezed out if there is not enough to go around.

Non-elite workers play a pivotal role in this system because their number is so large. These people are the chief customers for goods, such as homes, food, clothing, and transportation services. They also play a major role in paying taxes, and in receiving government services.

History says that if there are not enough resources to go around, we can expect increasing wage and wealth disparity. This happens because increased use of technology and more specialization are workarounds for many kinds of problems. As an economy increasingly relies on technology, the owners and managers of the technology start receiving higher wages, leaving less for the workers without special skills. The owners and managers also tend to receive income from other sources, such as interest, dividends, capital gains, and rents.

When there are not enough resources to go around, the temptation is to use technology to replace workers, because this reduces costs. Of course, a robot does not need to buy food or a car. Such an approach tends to push commodity prices down, rather than up. This happens because fewer workers are employed; in total they can afford fewer goods. A similar downward push on commodity prices occurs if wages of non-elite workers stagnate or fall.

If wages of non-elite workers are lower, governments find themselves in increasing difficulty because they cannot collect enough taxes for all of the services that they are asked to provide. History shows that governments often collapse in such situations. Major defaults on debt are another likely outcome (Figure 3). Pension holders are another category of recipients who are likely to be “left out” when the game of musical chairs stops.

Figure 3 – Created by Author.

The laws of physics strongly suggest that if we are reaching limits of this type, the economy will collapse. We know that this happened to many early economies. More recently, we have witnessed partial collapses, such as the Depression of the 1930s. The Depression occurred when the price of food dropped because mechanization eliminated a significant share of human hand-labor. While this change reduced the price of food, it also had an adverse impact on the buying-power of those whose jobs were eliminated.

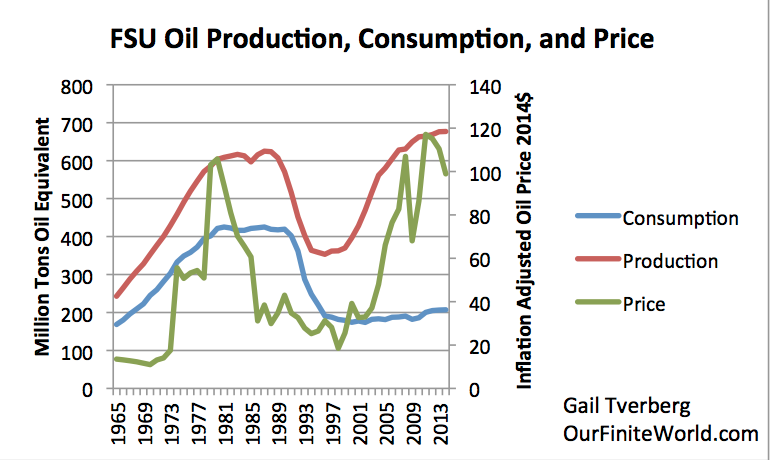

The collapse of the Soviet Union is another example of a partial collapse. This collapse occurred as a follow-on to the low oil prices of the 1980s. The Soviet Union was an oil exporter that was affected by low oil prices. It could continue to produce for a while, but eventually (1991) financial problems caught up with it, and the central government collapsed.

Figure 4. Oil consumption, production, and inflation-adjusted price, all from BP Statistical Review of World Energy, 2015.

Low prices are often a sign of lack of affordability. Today’s oil, coal, and natural gas prices tend to be too low for today’s producers. Low energy prices are deceptive because their initial impact on the economy seems to be favorable. The catch is that after a time, the shortfall in funds for reinvestment catches up, and production collapses. The resulting collapse of the economy may look like a financial collapse or a governmental collapse.

Oil prices have been low since late 2014. We do not know how long low prices can continue before collapse. The length of time since oil prices have collapsed is now three years; we should be concerned.

Myth 2. (Related to Myth 1) If we wait long enough, renewables will become affordable.

The fact that wage disparity grows as we approach limits means that prices can’t be expected to rise as we approach limits. Instead, prices tend to fall as an increasing number of would-be buyers are frozen out of the market. If in fact energy prices could rise much higher, there would be huge amounts of oil, coal and gas that could be extracted.

Figure 5. IEA Figure 1.4 from its World Energy Outlook 2015, showing how much oil can be produced at various price levels, according to IEA models.

There seems to be a maximum affordable price for any commodity. This maximum affordable price depends to a significant extent on the wages of non-elite workers. If the wages of non-elite workers fall (for example, because of mechanization or globalization), the maximum affordable price may even fall.

Myth 3. (Related to Myths 1 and 2) A glut of oil indicates that oil limits are far away.

A glut of oil means that too many people around the world are being “frozen out” of buying goods and services that depend on oil, because of low wages or a lack of job. It is a physics problem, related to ice being formed when the temperature is too cold. We know that this kind of thing regularly happens in collapses and partial collapses. During the Depression of the 1930s, food was being destroyed for lack of buyers. It is not an indication that limits are far away; it is an indication that limits are close at hand. The system can no longer balance itself correctly.

Myth 4: Wind and solar can save us.

The amount of energy (other than direct food intake) that humans require is vastly higher than most people suppose. Other animals and plants can live on the food that they eat or the energy that they produce using sunlight and water. Humans deviated from this simple pattern long ago–over 1 million years ago.

Unfortunately, our bodies are now adapted to the use of supplemental energy in addition to food. The use of fire allowed humans to develop differently than other primates. Using fire to cook some of our food helped in many ways. It freed up time that would otherwise be spent chewing, providing time that could be used for tool making and other crafts. It allowed teeth, jaws and digestive systems to be smaller. The reduced energy needed for maintaining the digestive system allowed the brain to become bigger. It allowed humans to live in parts of the world where they are not physically adapted to living.

In fact, back at the time of hunter-gatherers, humans already seemed to need three times as much energy total as a correspondingly sized primate, if we count burned biomass in addition to direct food energy.

Figure 6 – Created by author.

“Watts per Capita” is a measure of the rate at which energy is consumed. Even back in hunter-gatherer days, humans behaved differently than similar-sized primates would be expected to behave. Without considering supplemental energy, an animal-like human is like an always-on 100-watt bulb. With the use of supplemental energy from burned biomass and other sources, even in hunter-gatherer times, the energy used was equivalent to that of an always-on 300-watt bulb.

How does the amount of energy produced by today’s wind turbines and solar panels compare to the energy used by hunter-gatherers? Let’s compare today’s wind and solar output to the 200 watts of supplemental energy needed to maintain our human existence back in hunter-gatherer times (difference between 300 watts per hour and 100 watts per hour). This assumes that if we were to go back to hunting and gathering, we could somehow collect food for everyone, to cover the first 100 watts per hour. All we would need to do is provide enough supplemental energy for cooking, heating, and other very basic needs, so we would not have to deforest the land.

Conveniently, BP gives the production of wind and solar in “terawatt hours.” If we take today’s world population of 7.5 billion, and multiply it by 24 hours a day, 365.25 days per year, and 200 watts, we come to needed energy of 13,149 terawatt hours per year. In 2016, the output of wind was 959.5 terawatt hours; the output of solar was 333.1 terawatt hours, or a total of 1,293 terawatt hours. Comparing the actual provided energy (1,293 tWh) to the required energy of 13,149 tWh, today’s wind and solar would provide only 9.8% of the supplemental energy needed to maintain a hunter-gatherer level of existence for today’s population.

Of course, this is without considering how we would continue to create wind and solar electricity as hunter-gatherers, and how we would distribute such electricity. Needless to say, we would be nowhere near reproducing an agricultural level of existence for any large number of people, using only wind and solar. Even adding water power, the amount comes to only 40.4% of the added energy required for existence as hunter gatherers for today’s population.

Many people believe that wind and solar are ramping up rapidly. Starting from a base of zero, the annual percentage increases do appear to be large. But relative to the end point required to maintain any reasonable level of population, we are very far away. A recent lecture by Energy Professor Vaclav Smil is titled, “The Energy Revolution? More Like a Crawl.”

Myth 5. Evaluation methods such as “Energy Returned on Energy Invested” (EROI) and “Life Cycle Analyses (LCA)” indicate that wind and solar should be acceptable solutions.

These approaches are concerned about how the energy used in creating a given device compares to the output of the device. The problem with these analyses is that, while we can measure “energy out” fairly well, we have a hard time determining total “energy in.” A large share of energy use comes from indirect sources, such as roads that are shared by many different users.

A particular problem occurs with intermittent resources, such as wind and solar. The EROI analyses available for wind and solar are based on analyses of these devices as stand-alone units (perhaps powering a desalination plant, on an intermittent basis). On this basis, they appear to be reasonably good choices as transition devices away from fossil fuels.

EROI analyses don’t handle the situation well when there is a need to add expensive infrastructure to compensate for the intermittency of wind and solar. This situation tends to happen when electricity is added to the grid in more than small quantities. One workaround for intermittency is adding batteries; another is overbuilding the intermittent devices, and using only the portion of intermittent electricity that comes at the time of day and time of year when it is needed. Another approach involves paying fossil fuel providers for maintaining extra capacity (needed both for rapid ramping and for the times of year when intermittent resources are inadequate).

Any of these workarounds is expensive and becomes more expensive, the larger the percentage of intermittent electricity that is added. Euan Mearns recently estimated that for a particular offshore wind farm, the cost would be six times as high, if battery backup sufficient to even out wind fluctuations in a single month were added. If the goal were to even out longer term fluctuations, the cost would no doubt be higher. It is difficult to model what workarounds would be needed for a truly 100% renewable system. The cost would no doubt be astronomical.

When an analysis such as EROI is prepared, there is a tendency to leave out any cost that varies with the application, because such a cost is difficult to estimate. My background is in actuarial work. In such a setting, the emphasis is always on completeness because after the fact, it will become very clear if the analyst left out any important insurance-related cost. In EROI and similar analyses, there is much less of a tieback to the real world, so an omission may never be noticed. In theory, EROIs are for multiple purposes, including ones where intermittency is not a problem. The EROI modeler is not expected to consider all cases.

Another way of viewing the issue is as a “quality” issue. EROI theory generally treats all types of energy as equivalent (including coal, oil, natural gas, intermittent electricity, and grid-quality electricity). From this perspective, there is no need to correct for differences in types of energy output. Thus, it makes perfect sense to publish EROI and LCA analyses that seem to indicate that wind and solar are great solutions, without any explanation regarding the likely high real-world cost associated with using them on the electric grid.

Myth 6. Peer reviewed articles give correct findings.

The real story is that peer reviewed articles need to be reviewed carefully by those who use them. There is a very significant chance that errors may have crept in. This can happen because of misinterpretation of prior peer reviewed articles, or because prior peer reviewed articles were based on “thinking of the day,” which was not quite correct, given what has been learned since the article was written. Or, as indicated by the example in Myth 5, the results of peer reviewed articles may be confusing to those who read them, in part because they are not written for any particular audience.

The way university research is divided up, researchers usually have a high level of specialized knowledge about one particular subject area. The real world situation with the world economy, as I mentioned in my discussion of Myth 1, is that the economy is a self-organized networked system. Everything affects everything else. The researcher, with his narrow background, doesn’t understand these interconnections. For example, energy researchers don’t generally understand economic feedback loops, so they tend to leave them out. Peer reviewers, who are looking for errors within the paper itself, are likely to miss important feedback loops as well.

To make matters worse, the publication process tends to favor results that suggest that there is no energy problem ahead. This bias can come through the peer review process. One author explained to me that he left out a certain point from a paper because he expected that some of his peer reviewers would come from the Green Community; he didn’t want to say anything that might offend such a reviewer.

This bias can also come directly from the publisher of academic books and articles. The publisher is in the business of selling books and journal articles; it does not want to upset potential buyers of its products. One publisher made it clear to me that its organization did not want any mention of problems that seem to be without a solution. The reader should be left with the impression that while there may be issues ahead, solutions are likely to be found.

In my opinion, any published research needs to be looked at very carefully. It is very difficult for an author to move much beyond the general level of understanding of his audience and of likely reviewers. There are financial incentives for authors to produce PC reports, and for publishers to publish them. In many cases, articles from blogs may be better resources than academic articles because blog authors are under less pressure to write PC reports.

Myth 7. Climate models give a good estimate of what we can expect in the future.

There is no doubt that climate is changing. But is all of the hysteria about climate change really the correct story?

Our economy, and in fact the Earth and all of its ecosystems, are self-organized networked systems. We are reaching limits in many areas at once, including energy, fresh water, the number of fish that can be extracted each year from oceans, and metal ore extraction. Physical limits are likely to lead to financial problems, as indicated in Figure 3. The climate change modelers have chosen to leave all of these issues out of their models, instead assuming that the economy can continue to grow as usual until 2100. Leaving out these other issues clearly can be expected to overstate the impact of climate change.

The International Energy Agency is very influential with respect to which energy issues are considered. Between 1998 and 2000, it did a major flip-flop in the importance of energy limits. The IEA’s 1998 World Energy Outlook devotes many pages to discussing the possibility of inadequate oil supplies in the future. In fact, near the beginning, the report says,

Our analysis of the current evidence suggests that world oil production from conventional sources could peak during the period 2010 to 2020.

The same report also mentions Climate Change considerations, but devotes many fewer pages to these concerns. The Kyoto Conference had taken place in 1997, and the topic was becoming more widely discussed.

In 1999, the IEA did not publish World Energy Outlook. When the IEA published the World Energy Outlook for 2000, the report suddenly focused only on Climate Change, with no mention of Peak Oil. The USGS World Petroleum Assessment 2000 had recently been published. It could be used to justify at least somewhat higher future oil production.

I will be the first to admit that the “Peak Oil” story is not really right. It is a halfway story, based on a partial understanding of the role physics plays in energy limits. Oil supply does not “run out.” Peak Oilers also did not understand that physics governs how markets work–whether prices rise or fall, or oscillate. If there is not enough to go around, some of the would-be buyers will be frozen out. But Climate Change, as our sole problem, or even as our major problem, is not the right story, either. It is another halfway story.

One point that both Peak Oilers and the IEA missed is that the world economy doesn’t really have the ability to cut back on the use of fossil fuels significantly, without the world economy collapsing. Thus, the IEA’s recommendations regarding moving away from fossil fuels cannot work. (Shifting energy use among countries is fairly easy, however, making individual country CO2 reductions appear more beneficial than they really are.) The IEA would be better off talking about non-fuel changes that might reduce CO2, such as eating vegetarian food, eliminating flooded rice paddies, and having smaller families. Of course, these are not really issues that the International Energy Association is concerned about.

The unfortunate truth is that on any difficult, interdisciplinary subject, we really don’t have a way of making a leap from lack of knowledge of a subject, to full knowledge of a subject, without a number of separate, partially wrong, steps. The IPCC climate studies and EROI analyses both fall in this category, as do Peak Oil reports.

The progress I have made on figuring out the energy limits story would not have been possible without the work of many other people, including those doing work on studying Peak Oil and those studying EROI. I have also received a lot of “tips” from readers of OurFiniteWorld.com regarding additional topics I should investigate. Even with all of this help, I am sure that my version of the truth is not quite right. We all keep learning as we go along.

There may indeed be details of this particular climate model that are not correct, although this is out of my area of expertise. For example, the historical temperatures used by researchers seem to need a lot of adjustment to be usable. Some people argue that the historical record has been adjusted to make the historical record fit the particular model used.

There is also the issue of truing up the indications to where we are now. I mentioned the problem earlier of EROI indications not having any real world tie; climate model indications are not quite as bad, but they also seem not to be well tied to what is actually happening.

Myth 8. We don’t need religion; our leaders are all knowing and all powerful.

We are fighting a battle against the laws of physics. Expecting our leaders to win in the battle against the laws of physics is expecting a huge amount. Some of the actions of our leaders seem extraordinarily stupid. For example, if falling interest rates have postponed peak oil, then proposing to raise interest rates, when we have not fixed the underlying oil depletion problem, seems very ill-advised.

Everything I have seen indicates that there is a literal Higher Power governing our world economy. It is the Laws of Physics that govern the world economy. The Laws of Physics affect the world economy in many ways. The economy is a dissipative structure. Energy inputs allow the economy to remain in an “out of equilibrium state” (that is, in a growing state), for a very long period.

Eventually the ability of any economy to grow must come to an end. The problem is that it requires increasing amounts of energy to fight the growing “entropy” (higher energy cost of extraction, need for growing debt, and rising pollution levels) of the system. The economy must come to an end, just as the lives of individual plants and animals (which are also dissipative structures) must come to an end.

People throughout the ages have been in awe of how this system that provides growth works. We get energy from the sun. This solar energy helps grow our food. It allows the physical growth of humans. It allows the growth of ecosystems and of economies. Humans, ecosystems, and economies seem permanent, but eventually they all must collapse. In physics terms, they are all dissipative structures.

Humans have been in awe of the self-organizing property permitted by flows of energy for as long as humans have had the ability to think abstract thoughts. These flows allow a newly created whole to be greater than the sum of their parts. For example, babies start from a small beginning and mature into adults. Musical notes go together to form recognizable melodies. Physical movements go together to form dances. Awe for this phenomenon seems to be one of the origins of religion.

Another reason for religions is a need for hierarchical structure within an economy. We know that animal groups very often have “pecking orders.” Adding a god provides a convenient way of adding a “top level” to the pecking order. Of course, if leaders can convince members of the group that they are all knowing and that science can provide all of the answers, then the top level provided by religion is not needed.

A third reason for religions is to help align the thoughts of members in a particular way. Most of us are aware of the power of magnetized materials.

To some extent, the same power exists when the belief systems of groups of people can be aligned in the same direction. For example, teachers find it much easier to teach large groups of students, if parents have emphasized the importance of school and the need for respect for teachers. A military leader can attack another country, if soldiers follow orders. A group of generally uncivilized people can learn the benefit of working with others, if proper instruction is given.

What has been astounding to me, as I have looked into the situation, is that the scientific evidence seems to point in the direction of a literal Higher Power governing our Universe. It is not clear whether this higher power is the Laws of Physics, or whether it is some outside “God” that created the Laws of Physics.

In the past, many researchers assumed that the Universe was a closed energy system, irreversibly headed toward a cold, dark end. Recent research indicates that the Universe is ever-expanding, and in fact, seems to be expanding at an accelerating rate. While individual dissipative structures are constantly encountering more and more entropy, the universe as a whole is perhaps expanding rapidly enough to “outrun” growing entropy. Thus, it can behave as an always-open system. This always-open energy system allows many types of objects to self-organize and grow, at least for a time. These objects behave as dissipative structures, each having a beginning and an end.

We really don’t know whether the Universe had a beginning. Some research suggests that it did not. Others believe it began with a Big Bang.

Within the Universe, the earth seems extremely unusual. In fact, it is not clear that there is any other planet that has exactly the right conditions for complex life. A recent American Scientist article discusses this issue. The book Rare Earth: Why Complex Life Is Uncommon in the Universe points out the huge number of coincidences that were necessary for complex life to form and flourish.

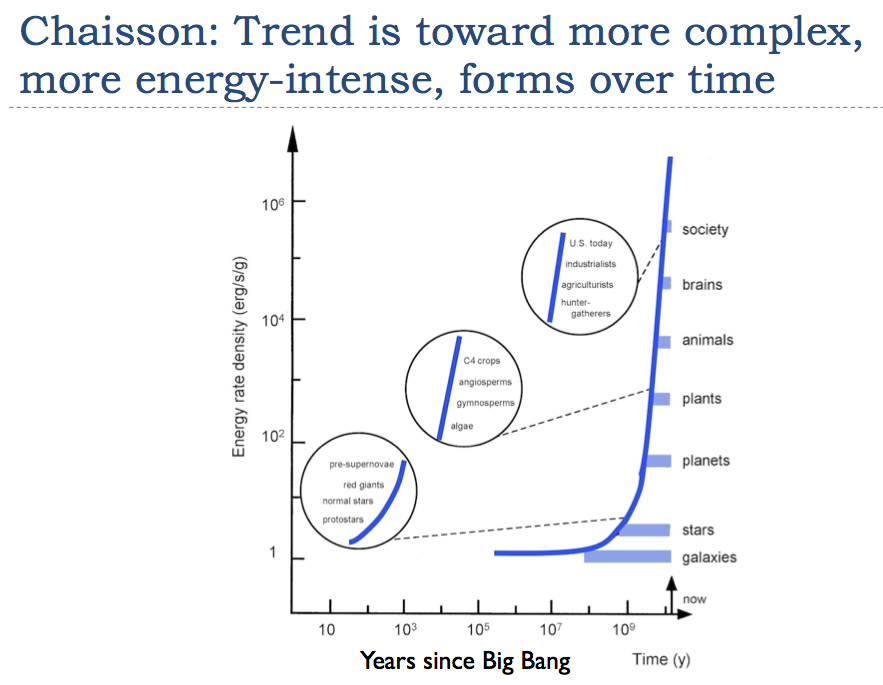

Within the Earth, and perhaps within the Universe as a whole, human economies are the most energy-dense form of structure found.

Figure 8. Image similar to ones shown in Eric Chaisson’s 2001 book, Cosmic Evolution: The Rise of Complexity in Nature.

Thus, in some sense, we humans and our economies may, in some sense, represent the current upper bound on development in the Universe.

We humans live on Earth. It is easy for us to think that our primary purpose in life is to care for and protect the Earth. Unfortunately, with our need for supplemental energy, this is not possible. Even at an early date, our need for resources exceeded what was sustainable. Joshua (in Joshua 17:14-18 relating to the period around 1400 BCE) instructs the tribes of Joseph to clear the trees from the hill country to have enough land for his tribe. This practice was clearly unsustainable; it would lead to erosion of the soil on hilltops. Even at that early date, high population and the need for resources to provide for this high population was conflicting with earth’s sustainability.

If our God is either the Laws of Physics, or some force giving rise to the Laws of Physics, then our God is really the God of the Universe. The limitations of the current Earth are no problem. God (or the Laws of Physics) could create a new Earth, or 1 million new Earths, if He chose to. Thus, from God’s point of view, it is not clear that there is any point to today’s environmentalism. There is a need not to poison ourselves, but “saving the earth” for other species after humans, or for a new set of humans who somehow will use much less energy, doesn’t make much sense. Humans can’t use much less energy; even if we could, our energy use would always be on an upward slope, headed to precisely where we are now.

There are many things that we can’t know for certain. Does this God want/expect us to worship him? Does this God plan an afterlife for some or all of the humans on Earth today? Obviously, if God (or the Laws of Physics) could create the Earth, God could also create other structures as well–possibly a “Heaven.” It is not clear to me that any one of today’s religions has a monopoly on insights regarding what is expected. A person might argue that we need not worry about religion at all, except for the fellowship it provides and the insights it offers regarding how early people coped with their difficulties.

Myth 9. The texts of religious groups around the world are literally true.

The texts of religious groups are true in the same sense that peer reviewed scientific literature is true. They represent, more or less, the best thinking of the day on a particular subject. This certainly does not mean that they are literally true.

We need to read religious texts in the context that they were written. In the earliest days, religious texts represented stories that people passed down from one generation to the next. These stories represented insights that these early people had gained. No one at that time was too concerned about authorship. If a story says, “God said,” it could also mean, “We think that this is something that God might have said.”

Literary styles were very different, back in an era before people pretended to have scientific knowledge. People created stories illustrating some aspect of a particular phenomenon. These stories were not supposed to fully describe what happened. This is why Genesis features two different creation stories.

The Bible makes liberal use of hyperbole and exaggeration. It is hard for people who are not familiar with the original language to understand how stories were intended to be interpreted. Is the concept of Hell added, primarily to provide a contrast to Heaven? In the Old Testament, the number of words in the ancient Hebrew language is much smaller than in today’s languages. This, by itself, makes direct translation difficult.

The earliest religious stories explained how God was perceived at that time. As people became more settled, their views changed. People were getting more “civilized.” Population densities were rising. The best beliefs in an early period may not have had relevance for a later period. This is why most religions have had reformers. Sometimes new writings are added. At other times, the way the writings are interpreted changes. This is why there seems to be a bizarre progression of stories from the Old Testament to the New Testament; new stories needed to be added to supplement and replace old ways of thinking.

Some of the things that early people discovered have not been understood by environmentalists. Genesis 1:28 says,

God blessed them and said to them, “Be fruitful and increase in number; fill the earth and subdue it. Rule over the fish in the sea and the birds in the sky and over every living creature that moves on the ground.”

The early people had figured out that humans were indeed different from other animals and plants. Their use of supplemental energy gave them power over other creatures. Their numbers could (and indeed, did) increase. Early authors were documenting how the world really worked. We later humans have been too blind to see the real situation. It is more pleasant for us to think that somehow we are just like other animals, except perhaps smarter and more in control. With our greater knowledge, we could somehow have avoided an increase in our numbers, if we had only planned better. The laws of physics say this cannot happen; our higher energy use dictates who will win the battle for resources.

The early religious stories were not too different from Peak Oil and Climate Change. They were sort of right. They gave partial insight. They were the best the authors could do at the time.

The ancient religious documents could not tell the whole story at once. New groups would gradually add more insights to the developing story, providing a better understanding of what was truly important for people living in a later period.

Conclusion

In practice, people need a religion or a religion-substitute. People need a basic set of beliefs with which to order their lives.

Our leaders today have proposed the Religion of Success, with its belief in Science, and the power of today’s leaders, as the new religion. This religion has appeal, because it denies the limits we are up against. Life will continue, as if we lived on a flat earth with unlimited resources. This story is pleasant, but unfortunately not true.

Donald Trump, with his version of conservatism, presents another religion. This religion seems to be focused on justifying the allocation of wealth away from the poor, toward the rich, through tax breaks for corporations and the wealthy. This is part of the process of “freezing out” the poor people of the world, when there are not enough resources to go around.

It is hard for me to support Trumpism, even though I recognize that in the animal world, the expected outcome when there are not enough resources to go around is “survival of the best-adapted.” If our concern is leaving energy resources in the ground for future generations, transferring buying power from the poor to the rich is a way of collapsing the economy quickly, while considerable resources remain in the ground. The fact that wealthy people are favored ensures that at least some people will survive.

China and Japan both have what are close to state religions, created by their leaders. School children learn stories regarding what is important, based on what state leaders tell them. In Japan, school children visit religious sites, and learn the proper religious observances. They also learn rules about what is expected of them–always be polite; respect those in charge; don’t eat food on the street; never leave any food wrappers on the ground. In many ways, these religions are probably not too different from today’s Religion of Success.

I personally am not in favor of religions that originate from political groups. I would prefer the “old fashioned” religions based on ancient documents from one or another of the world’s religions. We are clearly facing a difficult time ahead. Perhaps early people had insights regarding how to deal with troubled times. Admittedly, we don’t know for certain that heaven can be in our future. But when things look bleak, it is helpful to see the possibility of a reasonable outcome.

Furthermore, religious groups offer the possibility of finding a group of like-minded individuals to make friends with. We need all of the support we can get as we go through troubled times.