Back in June, one of Wall Street"s more philosophical derivatives strategists, DB"s Aleksandar Kocic looked at the state of the market and postulated that far from "stable" the existing risk "equilibrium" is one which can be described as "metastable", the result of widespread complacency, and which he compared to an avalanche where "a totally innocuous event can trigger a cataclysmic event (e.g. a skier’s scream, or simply continued snowfall until the snow cover is so massive that its own weight triggers an avalanche." Putting it in his usual post-modernist style, Kocic said that "complacency encourages bad behavior and penalizing dissent – there is a negative carry for not joining the crowd, which further reinforces bad behavior."

This is the source of the positive feedback that triggers occasional anxiety attacks, which, although episodic, have the potential to create liquidity problems. Complacency arises either when everyone agrees with everyone else or when no one agrees with anyone. In these situations, which capture the two modes of recent market trading, current and the QE period, the markets become calm and volatility selling and carry strategies define the trading landscape. But, calm makes us worry, and persistent worrying causes fear, and fear tends to be reinforcing.

Kocic framed the current state of the market as follows:

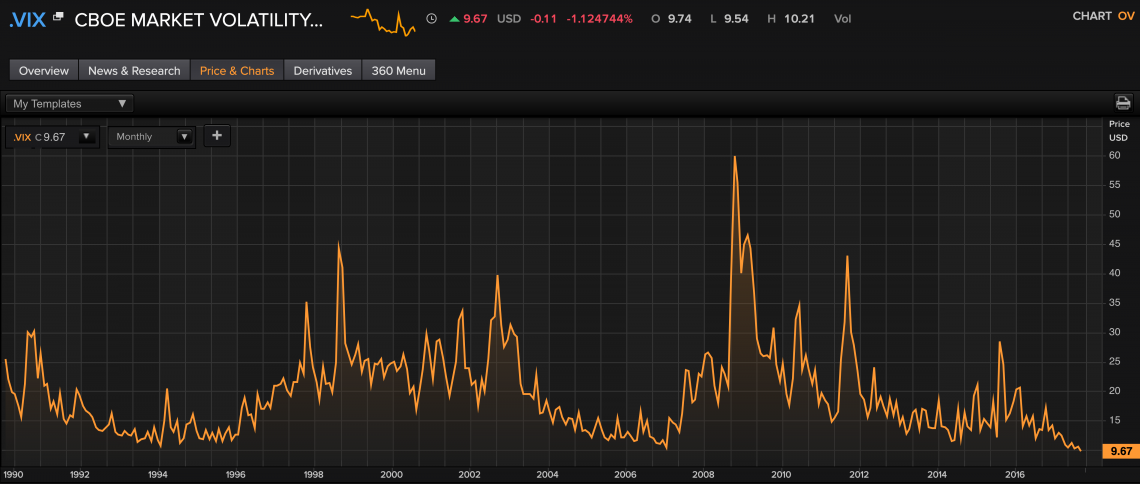

Unfortunately, the relentless grind ever lower in volatility, which as reported yesterday has resulted in both the lowest average September VIX on record...

... as well as the lowest September monthly settlement on record and only the second sub-10 monthly settlement...

... appears to have finally unsettled Kocic" expectations, even if ever so tacitly implied, for a spike higher in suppressed vol, and as he writes in his latest ruminations on volatility, "as volatility continues to be unfazed by what lies ahead in the near term, short of surprises in inflation, we are likely to linger at low levels."

Following up to his note from last week, which explained how the Fed"s fake "transparency" killed long-term investor, Kocic writes that "as transparency became the word of the decade, by its very nature it created the forces that push everything to the surface. Things exist thanks only to the attention they produce. There is no room for ambiguity."

Which ties in to the current news cycle, a relentless barrage of flashing red headlines, one scarier than the other, yet which on aggregate have zero adverse impact on volatility, and certainly on risk assets, which on Friday spiked to a new all time high following the latest last-second VIX-smash. Or, as Kocic puts it, "although shocks (political and other) keep arriving in the market, they seem to be appearing at what looks like predictable time intervals (usually, on Fridays). Practically every week, there is a new issue that eclipses the previous one, and we lose interest in past issues, before there is any semblance of resolution."

And with traders" attention spans already severely lacking, this habituation to hyperbolic, staccato newsflow means that not only is the market not discounting the future as Matt King postulated several months ago, but it is no longer able to even respond to the present, to wit:

Shocks, if they are predictable, lose their spell and gradually become facts of life. Predictable political shocks feed back into their source. Due to their antagonistic character, they gradually erode the ability to make consensus and reduce the ability to legislate, making further reforms at least questionable, if not highly unlikely. The market “euphoria” (aka the Trump trade) that followed immediately after the elections is being perceived as increasingly remote. Despite all the promises of reflation of the economy, fiscal stimulus, expectation of economic turnaround, no change is on the horizon. We are stuck with the status quo, albeit a noisy one.

So what does this mean for risk assets, and markets? According to the Deutsche analyst, "despite all the distortions and disruptions introduced by the central banks’, which has created a semi-permanent state of exception, markets have not lost one main characteristic, their adaptability. As the markets are getting inoculated against event risk, volatility continues to be under pressure. While we are distancing ourselves from the idea of political change, the Fed is seen, once again, as the main source of volatility. However, the Fed’s position is an uncomfortable one. The main problem it faces is the balance between preventing inflation from becoming a risk while at the same time not causing a rapid and substantial rise of rates. This requires a high level of fine tuning. It means that the Fed has to continue with rate hikes, but the hikes have to be done carefully without triggering the bond unwind."

The implication for vol traders is that contrary to warnings of market "metastability" and "suppressed cataclysmic vol events", Kocic - in many ways pulling a Hugh Hendry of his own - comes to the admission that fighting the Fed"s control over vol has become a futile pastime, and even though further complacency is in the cards, "continued vol selling" is encouraged.

... the market gradually, and reluctantly, trails behind the Fed, one hike at a time, and adjusts expectations on the go, without taking a longterm view on the Fed. It is difficult to see how this can lead to any excitement capable of inspiring higher volatility. As long as things evolve according to this scenario, everything shoiuld remain “predictable” with occasional noise that the market has learned to ignore. This is an environment that is bearish for volatility. It fosters further complacency and encourages continued vol selling.

Finally, Kocic takes a "Greek" detour and asks whether in this environment, in which every shock is ignored by a market now programmed to sell vol no matter what, "there is hope for Gamma?" Here is his answer:

In our recent publications, we have extracted one possible measure of liquidity from the volume data of Treasury futures. This measure quantifies sensitivity of the price to changes in trading volume. The liquidity index is expressed as a negative log of this sensitivity, so that large sensitivity corresponds to low liquidity and vice versa. The figure shows the (smoothed) liquidity (on the inverted axis) overlaid with the 3M10Y– low vol goes hand in hand with high liquidity.

Liquidity has a logical connection with volatility. This starts at the very short end and propagates across the term structure: By making a price, market makers are implicitly short volatility for which they are required to allocate risk capital and the bid/ask spread (which is an indirect measure of liquidity) is the compensation they receive for this risk exposure. All else equal, the ability to hedge an option is a function of liquidity of the underlying, and the option prices should reflect that. From the figure, we note that post 2004, with the disappearance of mortgage negative convexity hedging and the growth of volume on the exchanges, liquidity has been providing a lower bound for gamma – whenever gamma reached this lower bound, it has been pushed up. Also, the departures from that lower bound have been increasingly rarer and short lived. This holds not only for rates, but for equities as well.

As volatility continues to be unphased by what lies ahead in the near term, short of surprise in inflation, we are likely to linger at low levels. In that context, liquidity constraints are going to define the lower bound on gamma.

As a reminder, none of this is new: those who have traded this market (for more than just a few years) instead of merely commenting on it, will recall all those vol traders who lost their jobs in early 2007 when vol crashed so hard, there literally wasn"t a swaptions market. If Kocic is right, vol traders in 2017 (and perhaps 2018) will suffer the same fate. Of course, the 2007 episode is best remembered not for the the vol linked pink slips, but the explosion in VIX shortly thereafter and the resultant near collapse of the US financial system. Despite the Fed"s relentless pressure, trillions in liquidity injections and vol selling, we see nothing that has changed since then, and no reason why this time will be different.